Goals

- Before you can decide HOW you should invest your money, you first need to decide WHY you are investing your money.

- An investment plan that is tied to a long term goal such as saving for retirement decades down the road will need to look a lot different than a short term goal such as saving for a down payment on a house that you want to be able to purchase in 2 or 3 years.

- Generally, the longer the time frame you have to reach your investing goal, and the more money you need to pay for that goal, the more aggressive i.e. more risky your portfolio needs to be.

- The shorter the time frame, and the less amount of money you need for your goal, the more conservative, i.e. less risky your portfolio needs to be.

- Why is this?

Investment Risk Vs. Return

- Generally speaking, the riskier the investment, the greater the long term return it will achieve because people need to be able to expect higher returns in order for them to be willing to take on this additional risk. These types of riskier investments will have more volatility, and can have greater negative returns than more conservative investments over shorter time frames. But over longer time frames, they should generate higher returns.

- The more conservative the investment, the less likely you will experience negative returns, but because you aren't faced with the volatility of riskier investments, your returns will be lower and your portfolio wont grow as much over the long run.

- So using the previous examples, if you are decades away from retirement, the investments you use to fund your retirement goal need to be more aggressive. This is because you have enough time to ride out the ups and downs your portfolio will experience, and the greater long term returns will give you a better chance of having saved enough for retirement.

- If you are saving to purchase a house in 2 or 3 years, you can't afford to be too aggressive with how you invest those savings because you don't have time to recover from any losses that a more risky portfolio may experience.

Asset Allocation

- So what makes a portfolio more or less risky? It's asset allocation. The term asset allocation describes what percentages of your portfolio are allocated to the 3 main investment categories: Stocks, Bonds, and Cash (also referred to as short term investments).

- As you can see from the chart below, over time stocks have higher risk so they generate higher returns. Bonds have less risk so they generate lower returns than stocks. Cash or cash equivalents have the least amount of risk so they generate the least amount of return.

- As mentioned previously, a longer term goal should be assigned a portfolio allocation that has a higher percentage of stocks and a shorter term goal should have a portfolio allocation that has a higher percentage of bonds and cash.

Investments

- Once you have determined what percentages of your portfolio should be in the stocks, bonds, and cash categories, you then need to decide which individual investments you want to purchase in order to create a portfolio that has the desired mix.

- There are multiple ways to invest in stocks, bonds and cash, with mutual funds and exchange traded funds (ETF's) being two of the most popular ones.

- Mutual funds and ETF's allow you to purchase a basket of stocks or bonds all at once instead of having to go out and purchase them individually. This allows you to diversify your investments in a more simplified manner.

- When it comes to investment selection, we believe on focusing on what you can control. Cost is one of the few things you do have control over when it comes to investing.

- For this reason, whenever possible, we suggest using lower cost ETF's. In your employer-sponsored retirement accounts, ETF's are generally not available so try to focus on using low cost mutual funds when available. Does this mean you should ONLY choose the lowest cost option possible? No. We believe there are some actively managed funds and ETFs out there that may have slightly higher expense ratios as compared to passively managed options, y still can provide value.

Stay Disciplined

- Once you have implemented your portfolio with the asset mix and investments that align with your goals, the next step is the most challenging...

- Don't make emotional decisions to change the asset allocation of your portfolio unless your goals or situation has changed. For most people, this is easier said than done.

The 2020 Covid Crash and Rebound

First take a look at the chart above which reflects the year to date returns of the S&P 500 from January 1st through December 19th. The index dropped 33% between 2/19 and 3/25. Many investors panicked as the market started to experience a substantial decline in March. It's hard to knock them as they were only acting based on thousands of years of evolution that has hardwired our brains to be risk averse. The media knows this. So every time there is an event like this, they use fear-mongering to boost their ratings. This caused people to sell out of all of there investments at or towards the bottom of the stock market crash, essentially locking in there loss, \ and they never bought back in to reap the benefits of one of the fastest and largest stock market rebounds in history. As of 12/19, the major stock market indices are at or near all time highs.

This type of market correction and rebound has happened time and again. If fact, the market has ALWAYS rebounded after a substantial decline. Take a look at the char below which shows returns of the S&P 500 over the course of multiple negative political and economic events between 1999 and 2018. Think back to how you were feeling about your investments during each downturn. With each event, the media made it sound like the world was crashing down, but look how the markets performed over the long run.

- Experiencing these types of emotions when it comes to investing is completely normal. The key is managing them so that you don't make mistakes that could cost you dearly in the long run.

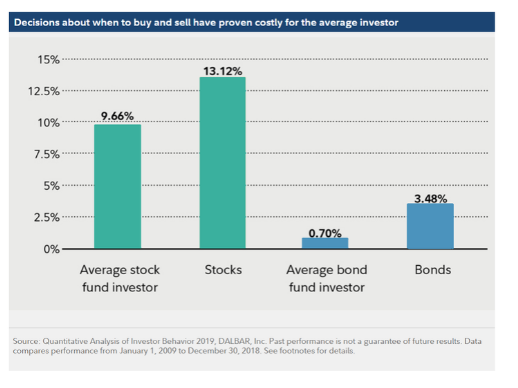

- The average fund investor tends to consistently under-perform the overall markets because their emotions cause them to buy and sell their investments at the worst possible times.

- They end up buying stocks at their peaks and selling at their bottoms.

- This cycle can lead to substantially lower returns than if they had just stuck with the original mix of stocks and bonds that made the most sense for their goals...

- Jumping in and out of the markets and missing only a few days of returns could cost you thousands...

Rebalancing

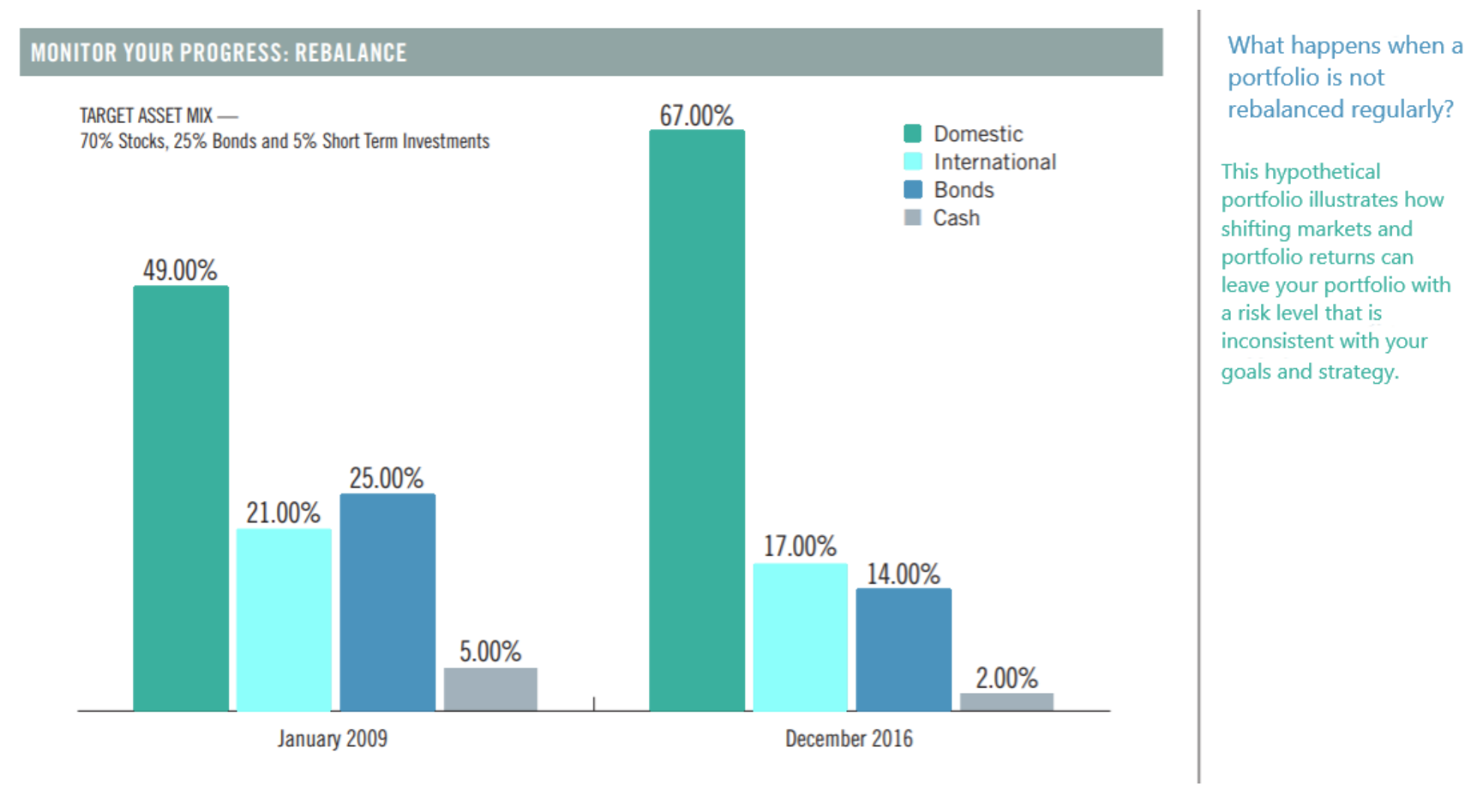

- If your goals or situation haven't changed, the only time you should make changes to your investments in your portfolio is when market fluctuations have steered your original intended asset allocation (and therefore your portfolio risk) off target.

- Rebalancing involves selling investments that have jumped in value and using the proceeds to buy investments that have not done as well. This may sound counter intuitive, but this actually helps you to buy low and sell high (good for returns) while keeping your original desired mix of stocks, bonds, and cash.

- In the below example you will see that during periods of high stock market returns, if you ignore your portfolio and never rebalance it, you will all of a sudden have a portfolio that has substantially more stock exposure and therefore risk, than you originally deemed appropriate.

Rebalancing Applies In Down Markets Also

- The opposite can happen during periods of stock market declines.

- During a stock market slump the individual stock holdings in your portfolio will lose value, which means you will find your overall portfolio containing a lower percentage of stocks and a higher percentage of conservative bonds. This makes your portfolio too conservative and reduces your ability to achieve the long term growth that you need to achieve your goals.

- Lets say for example you are supposed to have a 70/30 mix of stocks to bonds, but the stock market has under-performed recently and now your portfolio is at a 60/40 mix. The savvy investor would know to sell 10% of their bonds holdings (which haven't lost value like stocks because they are more conservative).

- They would then take the proceeds from selling those bonds and buy enough stocks (which are on sale) to bring their portfolio weightings back up to a 70/30 mix of stocks to bonds.

401(k) and 403(b) Contributions

- When it comes to deciding how to contribute to your employer-sponsored 401(k) or 403(b) there are a few things you need to know.

- You ALWAYS need to find out what your company match is. This is the percentage of your salary that your employer contributes on your behalf as long as you are making your own contributions. For example they may state that they will provide a dollar for dollar contribution up to 4%.

- This means if your salary is $100,000 and you are contributing 4% yourself, you will be putting $4,000 into your account over the course of the year and so will your employer. Since this is free money and basically a guaranteed 100% return on your contributions, you should always do everything possible to at least contribute enough to receive your full company match.

- Ideally, you are able to contribute a much higher percentage than that regardless of what the employer match percentage is. The more you save, the more likely it is you will be able to retire when you want to and a 4% contribution rate simply wont cut it.

- Nowadays, many employer plans are allowing you to make Roth Contributions. You need to find out if this is an option and decide if you should make your contributions in the form of Roth savings, or if it makes more sense to contribute in the more traditional manner of pre-tax contributions.

- What's the difference?

- Keep in mind that even if you contribute Roth money into your 401(k) or 403(b), your employer match will always be in the form of pre-tax dollars so it's common for people to have both types of money in their employer-sponsored retirement accounts.

- This is not an all or nothing choice. If your plan offers the option of Roth contributions, you can direct some of your contributions towards Roth, and some towards pre-tax contributions.

The 3 Methods for Selecting and Managing Your Investments In Your 401(k) or 403(b)

- So how do you actually go about selecting and then rebalancing the investments in your employer retirement accounts?

- Generally you have three options.

- One is not necessarily better than the other. It just comes down to how much expertise, experience, time, and desire you have to go through the investing process. In the following section we will break down all three options.

Option 1: The Self-Directed Approach

- This option is for those who need little or no help with their investments

- They are willing and able to spend the time necessary to research and select investments for their portfolio initially, as well as perform regular rebalancing.

- If you go this route, you would just pull up the menu of investment options in your plan, and designate what percentage of your portfolio you want to be in various individual funds.

- The biggest benefit of this approach is that you aren't paying any additional management fees aside from the individual expenses of each fund. You also have full control in customizing your portfolio.

- The biggest drawback to this approach is that it requires you to put in extra time that you may not have to be successful. And it also requires you to stay disciplined and avoid making any costly mistakes based on emotional reactions to the markets.

- Tip #1 for this approach: Some plans have free tools available to help you self direct your portfolio. They may offer an option to receive a model portfolio based on the answers you provide to their questionnaire. The model will recommend exactly how much of your portfolio should be invested in each plan investment option given your current situation. For example, it will come out and say you should have "X" percent of your portfolio in fund A, "X" percent in fund "B", and so on. While there is no additional charge for this, your portfolio will NOT be rebalanced for you. This means you would still need to monitor your portfolio after implementing the recommended strategy, and know what trades to make to keep it at the desired level of risk.

- Tip #2 for this approach: If you really are self-directed, and you truly enjoy going through the entire investment process, you may want to inquire if your plan offers an expanded menu of investment choices. For example, with plans serviced by Fidelity, you have your basic core investment options which usually consists of a set of mutual funds. But then some plans also offer what's called a Self-Directed Brokerage Link. This feature gives you access to invest your 401(k) or 403(b) money in additional fund options and sometimes even stocks. You have to separately sign up for this option.

- In my experience, most people do NOT have the time, experience, and willingness to properly self direct a portfolio in their 401(k) or 403(b). It's important to be honest with yourself if you decide to take this approach. I have seen countless examples of people who have decided to go this route with the best of intentions. They received a model portfolio, and implemented the recommended strategy, but then life got busy, and they forgot or simply neglected to rebalance and update their portfolio moving forward.

Option 2: Target Date Funds

- A Target Date Fund is a single fund approach to being diversified. That is because inside of this single fund, there is an allocation of other funds from all 3 major asset classes: Stocks, Bonds, and Short Term investments.

- This is more of a hands off approach to investing in your employer plan because the selection of investments and the rebalancing is done for you. Because of its simplicity, it's generally the default option. So if you start making contributions to a new 401(k) or 403(b), but you forget to make an investment selection for those contributions, this is where your money will most likely end up.

- Generally these funds come in 5 or 10 year increments. The idea is to choose the fund matched to the year that is closest to when you expect to retire. For example, you may see a list of target date fund options in your plan that are labeled Target Date 2020, Target Date 2030, Target Date 2040, and so on. If you expect to retire in 2048, the idea is that you would choose the 2050 fund. They may have their own unique names depending on what investment firm manages the funds. For example Fidelity calls their version of target date funds their Freedom Funds.

- As the years go by and you get closer to the target date of your selected fund, the asset mix inside of it becomes more and more conservative. This means that gradually and automatically, the fund will hold less and less in stocks and more and more in bonds and short term investments. So a 2050 target date fund will hold most of its money in stocks since that fund manager knows people who invest in that fund are young, so they can afford to take on more risk right now in exchange for higher returns. A 2020 target date fund will hold much less in stocks because that fund manager knows people who are invested in it, are at or close to retirement. So they can't afford to take on as much risk.

- The biggest benefit of this approach is that it requires less time and effort from the investor.

- The biggest drawback is that it is not a very customized approach. The fund manager decides how much risk you should take with your portfolio based on your age. That's it. They don't factor in anything else such as your income, other investment savings, and expenses. Two people who expect to retire in the same year could actually need a very different portfolio depending on their situation and target date funds don't account for those differences.

- Tips for this approach: Please, Please, Please, don't invest in more than one target date fund in your 401(k) or 403(b). I used to see this all the time. Someone would own 5 or 6 target date funds figuring they were being more diversified with their portfolio. The reality is that caused them to be LESS diversified. Why is this? Because those target date funds are actually funds of other funds, so they ultimately own stocks in a lot of the same companies, just with varying degrees based on the target retirement year. By owning multiple target date funds, you could end up being overly concentrated in one single company's stock which is never a good thing. Just being in the one target date fund should be enough to be properly diversified.

- Also be aware that not all target date funds are created equal. A 2050 fund being managed by Fidelity probably does not have the same ratio of stocks to bonds as a 2050 fund run by Vanguard. This means they have different levels of risk even though they are designed for the same target year. Long story short, know what you own.

Option 3: A Fully Managed Account

- Many 401(k) and 403(b) plans offer a managed account service. For example many Fidelity plans offer either Fidelity Portfolio Advisory Services at Work, or management through a third party, Financial Engines. When you enroll in a service like this, you are delegating the management of your portfolio to a third party professional.

- They will take care of selecting your asset allocation, choosing how much of each available investment option should be in your portfolio, and rebalancing.

- Because they are doing all the work for you, there is an extra fee associated with this. Generally, this fee is charged as a percentage of the dollar amount that is inside of your 401(k) or 403(b).

- Keep in mind that this percentage management fee is in addition to the individual underlying fund fees.

- But the additional fee may very well be worth it for people who do not have the time, expertise, or willingness to properly manage their own portfolio.

- The benefit of this option is that you are delegating your portfolio management to professionals. This helps to avoid some of the emotional investing mistakes that people tend to make on their own. Secondly, this option us usually more of a customized approach than target date funds as the portfolio manager will generally consider more details of your financial life when determining how your portfolio should be invested. Lastly, even though there is an additional management fee for this service, when it is inside of a 401(k) or 403(b), this fee is lower than you would usually pay for the management of an IRA.

- One drawback to this approach is the additional cost and the fact that you don't really have much say in how your portfolio is managed ( although this could be a good thing). Secondly, you are paying a professional for management, but when it comes to them selecting your investments, they are handcuffed to the menu of choices that your employer provides. So If your employer only gives you one or two options in each investment category, stocks, bonds, and short term, you may better off saving the management fee and using the free model portfolio tools to do it on your own.

Key Takeaways

- All investing involves some types of risk. The key to long term success is to focus on what you can control. This includes your investments costs and your asset allocation.

- The number one obstacle when it comes to achieving your investment goals, is not political or economic events, its you.

- Keeping your emotions in check and approaching your investment decisions methodically will lead to long term success.

- At HCP Wealth Planning, we recognize this is easier said than done. The best way to do this is to always fall back to the plan.

- When you determine what portfolios make the most sense for you and how they should tie into your overall plan, you need to factor in the various potential market incomes, including poor markets.

- If the markets are causing you stress you should revisit your overall plan and make sure nothing about your situation has changed that would cause you to want to reconsider the amount of risk in your investments.